Will the Rates Be Cut Again Soon?

Mortgage charge per unit forecast for next calendar week ( Apr 25-29 )

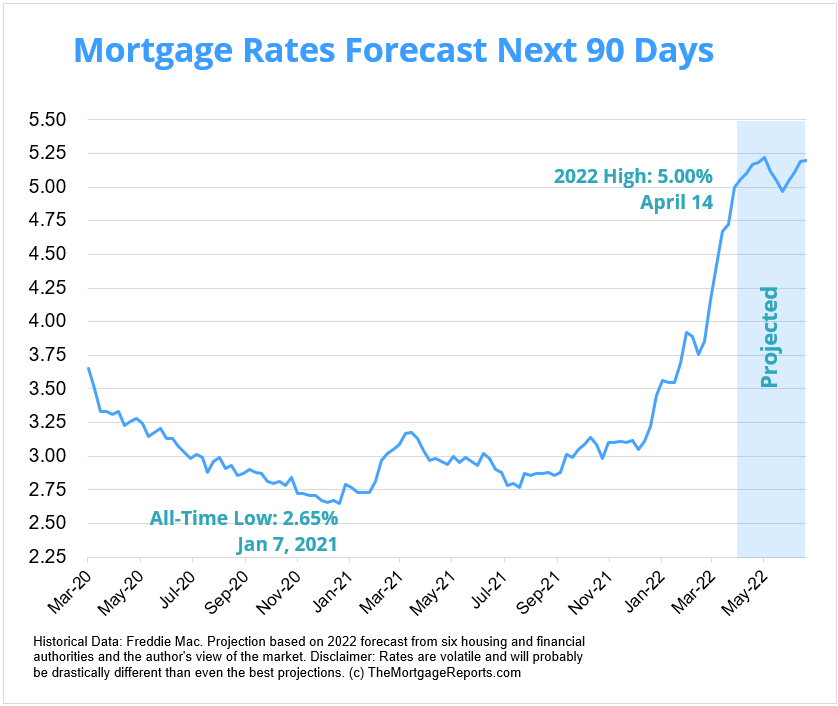

Soaring inflation and multiple planned hikes from the Federal Reserve pushed mortgage rates to a decade-high final week.

The average 30-twelvemonth fixed involvement charge per unit rose again, going from iv.72% on Apr vii to 5.00% on April 14. The last fourth dimension the weekly average reached the five% plateau was February. 2011.

Most interest rate indicators continue to betoken up, although a new Covid outbreak or the state of war in Ukraine becoming more unstable could cause variance and potentially some brusque-term declines.

In this article (Skip to...)

- Will rates get down in May?

- ninety-day forecast

- Expert rate predictions

- Mortgage rate trends

- Rates by loan type

- Mortgage strategies for May

- Mortgage rates FAQ

>Related: Cash-out refinance: Best uses for your dwelling house equity

Will mortgage rates get downwardly in May?

Mortgage rates surged through the first quarter of 2022. The 156 ground point (1.56%) gain represented the fastest three-month ascension since May 1994, according to Freddie Mac.

With the pandemic's declining economic impact, inflation running at 40-year highs, and the Federal Reserve outlining an aggressive policy plan, involvement rates could continue trending upwards.

Experts from the Mortgage Bankers Association, First American and other industry leaders expect 30-year mortgage rates to keep climbing in May — though perhaps not as chop-chop as they have over the past calendar month.

With the Fed signaling its rate-increase plans well in accelerate, mortgage markets take likely already priced in the bulk of the bear on.

Of class, the state of war in Europe or a fasten from a new Covid variant could cause interest rates to drop from week to calendar week.

"The path to higher rates may be bumpy, only the bulletin from the Fed is clear – aggressive tightening is necessary to tame aggrandizement."

—Odeta Kushi, deputy chief economist at First American

Nadia Evangelou , senior economist and director of forecasting at the National Clan of Realtors

Prediction: Rates will ascension

"The Federal Reserve will again raise its benchmark rate in May. With the unemployment rate virtually record lows and inflation the highest in four decades, the Federal Reserve may take a more aggressive rate hike this time, pushing up mortgage rates further.

I wait the thirty-year fixed mortgage rate to average v.ii% side by side month. Equally inflation will somewhen beginning slowing downwards subsequently this year, mortgage rates may not rise every bit fast as they do now. Thus, I expect the 30-twelvemonth fixed mortgage rates to average nearly 5% in 2022."

Daryl Fairweather , chief economist at Redfin

Prediction: Rates volition moderate

"Mortgage rates have already gone up to reflect the Fed's unwinding of its mortgage portfolio and its plans to heighten the federal funds charge per unit. If rates go upward more information technology will be because inflation remains out of control. But if the Fed does get a hold of inflation, it's possible rates could go down moderately. Nosotros'll have to expect and see."

Mike Fratantoni , primary economist at Mortgage Bankers Clan

Prediction: Rates will rising

"Given that we are past full employment and with aggrandizement running over viii% annually, our expectation is that the Federal Reserve will continue with rapid rate hikes this year, and for the Federal funds rate to attain a range of 2.25% to 2.5% past the end of 2022. Nosotros await the rate hikes to continue through mid-2023.

Additionally, the Fed will be announcing plans to reduce the size of their Treasury and MBS holdings at their upcoming meeting in May, quickly ramping up to reductions of $95 billion per calendar month. This will add additional volatility to the mortgage marketplace and will be another cistron keeping mortgage rates elevated.

The inflation moving picture and the signals of tightening from the Fed have pushed Treasury yields significantly college in contempo weeks and have added considerable volatility for mortgage rates. Our forecast is for the x-year Treasury yield to cease 2022 at around two.8% and remain at those levels through 2023, before falling to 2.five% in 2024. Mortgage rates are expected to finish 2022 at 4.viii% – and to decline gradually to 4.6% by 2024 – as spreads narrow."

Selma Hepp , deputy principal economist at CoreLogic

Prediction: Rates volition moderate

"Runaway inflation expectations are posing serious business organization for the Federal Reserve which has get increasingly more vocal almost its attempt to exist more aggressive in reining it in. As a result, we've seen a surge in mortgage rates significantly in a higher place levels where we expected at this point.

Some of the run upwards is a response to Fed's rest canvass reduction and some is apprehension of Fed's moves. Nevertheless, demand is starting to negatively respond to college rates which is likely to slow further mortgage rate increases. While rates will continue to oscillate, they are likely to remain effectually v% range."

Odeta Kushi , deputy chief economist at First American

Prediction: Rates volition rising

"The 30-year, fixed mortgage charge per unit has increased sharply and swiftly over the past several months, and the expectation is that rates will continue to ascension in May. The path to college rates may be bumpy, but the bulletin from the Fed is clear – ambitious tightening is necessary to tame inflation.

In add-on to Federal funds rate hikes, the Fed is expected to begin reducing its balance canvas as early equally May, and eventually may consider sales of bureau mortgage-backed securities (MBS), which will put direct upwards pressure on mortgage rates. Ongoing geopolitical uncertainty may prompt swings in the mortgage rate on a daily or weekly basis, but the trend for mortgage rates is notwithstanding to the upside."

Ralph McLaughlin , chief economist at Kukun

Prediction: Rates will ascension

"Recent signals from the Federal Reserve show that their principal monetary concern is getting this historically high inflation under control. As American households continue to get hammered on ascension costs seemingly everywhere, the markets expect the Fed to get more bullish.

That means the Fed may very well ditch the usual incremental interest rate raises of 25 basis points and raise rates by 50 bps in May. And if that doesn't do the trick, they will likely go another l bps again in mid-June."

Mortgage involvement rates forecast side by side xc days

Aside from dubiousness surrounding the Russian-Ukrainian conflict or a fasten in positive Covid cases warranting new restrictions, all other major indicators point toward further mortgage rate growth.

In all likelihood, average interest rates will increment over the next three months. Of course, mortgage rates tend to be volatile and then we could run into some drops mixed in also.

Mortgage rate predictions for 2022

The boilerplate xxx-year fixed rate mortgage ended 2021 at iii.1%, according to Freddie Mac.

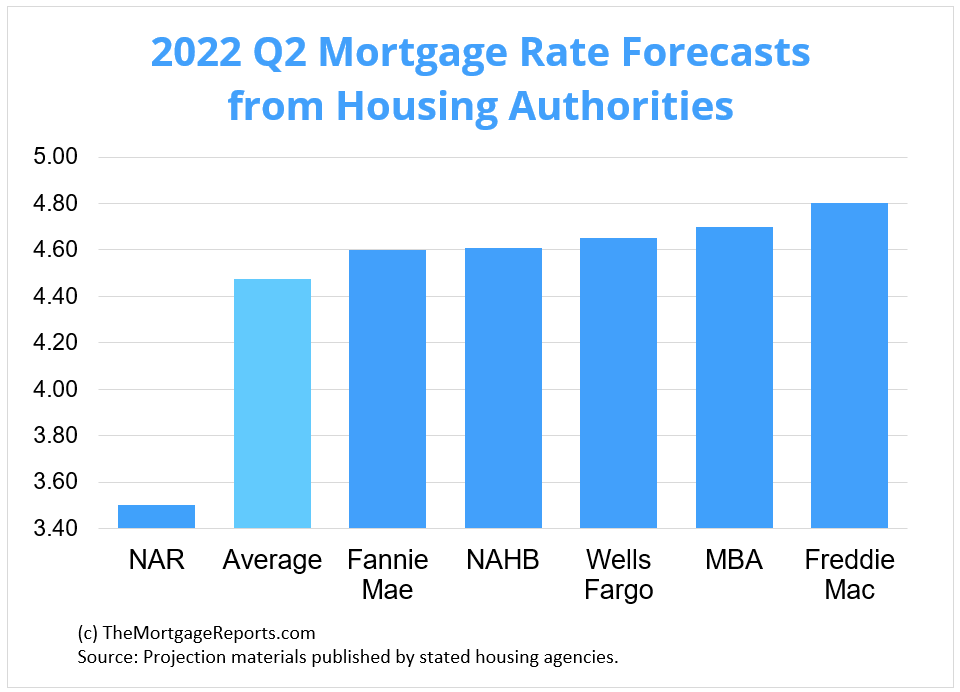

All vi of the major housing government nosotros gathered project that average to rise over the second quarter of 2022.

The National Clan of Realtors and Fannie Mae sit down at the low stop of the grouping, estimating the boilerplate thirty–twelvemonth fixed interest charge per unit will settle at iii.v% or 4.6% past the end of Q2. (Though, NAR's is likely due to its forecast lagging behind the others.) The Mortgage Bankers Clan and Freddie Mac had the highest predictions, with forecasts of 4.7% and 4.8%, respectively, past the end of June.

| Housing Potency | 30-Year Mortgage Charge per unit Forecast (Q2 2022) |

| National Association of Realtors | three.50% |

| Fannie Mae | 4.60% |

| National Association of Habitation Builders | 4.61% |

| Wells Fargo | 4.65% |

| Mortgage Bankers Clan | iv.70% |

| Freddie Mac | iv.eighty% |

| Boilerplate Prediction | 4.48% |

Current mortgage interest rate trends

Mortgage rates saw unprecedented growth in 2022's opening quarter and shot up to 11-year highs in Apr.

The average thirty-year fixed charge per unit jumped from 4.72% to 5.00% for the 7 days ending April 14, according to Freddie Mac'southward weekly rate survey.

Similarly, the 15–twelvemonth fixed rate rose from 3.91% to 4.17%, while the boilerplate rate for a 5/one ARM increased from 3.56% to three.69%.

| Calendar month | Average 30-Yr Fixed Charge per unit |

| April 2021 | 3.06% |

| May 2021 | two.96% |

| June 2021 | 2.98% |

| July 2021 | 2.87% |

| Baronial 2021 | 2.84% |

| September 2021 | 2.90% |

| October 2021 | 3.07% |

| November 2021 | 3.07% |

| Dec 2021 | 3.x% |

| Jan 2022 | iii.45% |

| Feb 2022 | three.76% |

| March 2022 | 4.17% |

Source: Freddie Mac

Mortgage rates moved on from the record–low territory seen in 2020 and 2021 merely are still low from a historical perspective.

Dating back to April 1971, the fixed xxx–year interest rate averaged vii.79%, co-ordinate to Freddie Mac.

So if yous haven't locked a rate all the same, don't lose also much sleep over information technology. You can still become a great deal — especially for borrowers with potent credit.

Just make sure you lot store effectually to detect the best lender and lowest charge per unit for your unique situation.

Mortgage charge per unit trends by loan type

Many mortgage shoppers don't realize there are different types of rates in today'due south mortgage market.

Merely this noesis tin aid home buyers and refinancing households find the best value for their situation.

Following are iii–calendar month mortgage rate trends for the almost pop types of home loans: conventional, FHA, VA, and jumbo.

| March 2022 | February 2022 | Jan 2022 | |

| Conforming Loan Rates | 4.79% | four.09% | 3.77% |

| FHA Loan Rates | 4.81% | four.eleven% | 3.86% |

| VA Loan Rates | iv.57% | three.77% | 3.56% |

| Colossal Loan Rates | 4.37% | 3.76% | 3.45% |

Source: Black Knight Originations Market place Monitor Report

Which mortgage loan is best?

The best mortgage for you depends on your financial situation and your goals.

For example, if you desire to buy a loftier–priced abode and you accept great credit, a jumbo loan is your best bet. Jumbo mortgages permit loan amounts above conforming loan limits – which max out at $647,200 in virtually parts of the U.S.

On the other mitt, if y'all're a veteran or service member, a VA loan is almost always the correct choice.

VA loans are backed by the U.Due south. Section of Veterans Affairs. They provide ultra–low rates and never charge private mortgage insurance (PMI). But y'all need an eligible service history to qualify.

Conforming loans and FHA loans (those backed past the Federal Housing Administration) are great low–down–payment options.

Conforming loans allow as little equally iii% down with FICO scores starting at 620.

FHA loans are even more lenient about credit; dwelling house buyers can frequently qualify with a score of 580 or higher, and a less–than–perfect credit history might not disqualify you.

Finally, consider a USDA loan if you desire to buy or refinance real estate in a rural area. USDA loans have below–market rates – similar to VA – and reduced mortgage insurance costs. The catch? Y'all need to live in a 'rural' area and have moderate or low income to be USDA–eligible.

Mortgage rate strategies for May 2022

Mortgage rates opened 2022 with huge and rapid growth. While the pace may tiresome, they're expected to go on climbing in May and through the rest of the year. But opportunities to lock in a low involvement rate do still exist for home buyers and refinancing homeowners.

Here are just a few strategies to continue in heed if you're mortgage shopping in the next few months.

The time to lock a rate is at present

The Federal Reserve is ready to raise its federal funds charge per unit target following each of the 6 remaining FOMC meetings this year. The key bank plans to do this as a counter to the country's historically high inflation and mortgage interest rates tend to grow in response.

While mortgage rates have spiked throughout the twelvemonth, the boilerplate 30-year fixed rate jumped 31 basis points (0.31%) immediately afterwards the FOMC meeting in March. The next two meetings are scheduled for May three-4 and June 14-fifteen.

While mortgage rates are notorious for their week-to-week volatility, nearly every indicator points to them growing over the rest of 2022.

If you're ready to buy a home or refinance, the sooner you lock in a rate, the better. Getting ahead of the game and lining up all your paperwork volition only assistance you to get approved faster.

Create a lower rate for yourself

No, you won't need a time automobile (or a crystal ball).

Getting the best involvement rate for your financial situation volition just take a trivial piece of work. While the growing rate environment hurts affordability, you tin also use it to your reward.

The year'due south rising rates decreased mortgage volume, which means lenders demand concern and are more than likely to compete for yours. Once you lot get a prequalified or qualified rate from i lender, accept the additional steps of shopping it around to others.

That competition will result in locking in a lower rate and potentially saving thousands of dollars over the lifetime of your loan.

How to compare interest rates

Rate shopping doesn't just mean looking at the lowest rates advertised online because those aren't available to everyone. Typically, those are offered to borrowers with perfect credit and who can put a down payment of xx% or more than.

The rate lenders actually offer depends on:

- Your credit score and credit history

- Your personal finances

- Your down payment (if buying a home)

- Your dwelling house disinterestedness (if refinancing)

- Your loan-to-value ratio (LTV)

- Your debt-to-income ratio (DTI)

To figure out what rate a lender tin can offer you based on those factors, yous have to fill out a loan application. Lenders will cheque your credit and verify your income and debts, then give you a 'real' rate quote based on your financial state of affairs.

You should go 3-five of these quotes at a minimum. Then compare them to observe the best offer.

Wait for the lowest rate, but too pay attending to your annual percentage charge per unit (APR), estimated closing costs, and 'discount points' — extra fees charged upfront to lower your rate.

This might audio like a lot of work. Simply you can store for mortgage rates in under a day if you put your mind to it. And shaving simply a few basis points off your rate can save you lot thousands.

Mortgage interest rate FAQ

What are current mortgage rates?

Current mortgage rates are averaging 5.00% for a 30–year fixed–rate loan, four.17% for a 15–year fixed–rate loan, and 3.69% for a 5/1 adjustable–rate mortgage, according to Freddie Mac'due south latest weekly charge per unit survey. Your individual rate could be higher or lower than the boilerplate depending on your credit score, down payment, and the lender you choose to work with, amidst other factors.

Will mortgage rates go downwards side by side week?

Mortgage rates could decrease next calendar week (April 25-29, 2022) depending on how the war in the Ukraine progresses. Though rates could rise if strong aggrandizement continues and the marketplace adjusts to upcoming Federal Reserve'due south rate hikes.

Volition mortgage interest rates go downwards in 2022?

It's unlikely mortgage rates volition become downwards in 2022. Inflation has been climbing at a record charge per unit over the final few months. And the Fed is planning to raise interest rates later each of its scheduled FOMC meetings. Both these factors should lead to significantly higher mortgage rates in 2022.

Will mortgage interest rates go up in 2022?

Yes, it'southward very probable mortgage rates will increase in 2022. High inflation, a strong housing market place, and policy changes by the Federal Reserve should all push button rates higher in 2022. The but affair likely to push rates down would exist a major resurgence in serious Covid cases and further economic shutdowns. But, while information technology could help mortgage rates, no one is hoping for that outcome.

What is the lowest mortgage rate right at present?

Freddie Mac is at present citing boilerplate 30–yr rates in the 5 percent range. If you can observe a rate in the 4s, you're in a very good position. Think that rates vary a lot by borrower. Those with perfect credit and large down payments may become below–average interest rates, while poor–credit borrowers and those with non–QM loans could encounter much college rates. You'll demand to become pre–approved for a mortgage to know your exact charge per unit.

Volition at that place be a housing crash in 2022?

For the well-nigh part, manufacture experts do not expect the housing market to crash in 2022. Yes, domicile prices are over–inflated. Only many of the risk factors that led to the 2008 crash are not present in today's marketplace. Low inventory and massive heir-apparent demand should keep the market propped upwardly next year. Plus, mortgage lending practices are much safer than they used to be. That means there'south non a subprime mortgage crunch waiting in the wings.

What is the everyman mortgage charge per unit e'er?

At the time of this writing, the everyman 30–twelvemonth mortgage charge per unit always was 2.65 per centum. That's according to Freddie Mac's Primary Mortgage Market Survey, the most widely–used benchmark for current mortgage interest rates.

Should I lock my rate now or look?

Locking your charge per unit is a personal decision. You should exercise what'south right for your situation rather than trying to time the market. If you're buying a domicile, the right time to lock a rate is after y'all've secured a purchase agreement and shopped for your best mortgage deal. If y'all're refinancing, you should make certain y'all compare offers from at least three to 5 lenders before locking a charge per unit. That said, rates are ascension. So the sooner you can lock in today's marketplace, the better.

Is now a good time to refinance?

That depends on your situation. It'due south a adept time to refinance if your current mortgage rate is above market rates and you could lower your monthly mortgage payment. It might also be skillful to refinance if you can switch from an adjustable–rate mortgage to a low fixed–charge per unit mortgage; refinance to become rid of FHA mortgage insurance; or switch to a short–term 10– or 15–year mortgage to pay off your loan early.

Is it worth refinancing for 1 pct?

It's oft worth refinancing for 1 percent signal, as this tin yield meaning savings on your mortgage payments and full interest payments. Just make sure your refinance savings justify your closing costs. You lot can apply a mortgage calculator or speak with a loan officer to crisis the numbers.

How do I shop for mortgage rates?

Start by choosing a listing of 3–5 mortgage lenders that you're interested in. Look for lenders with low advertised rates, great customer service scores, and recommendations from friends, family unit, or a real manor agent. And so get pre–approved by those lenders to run into what rates and fees they can offer you. Compare your offers (Loan Estimates) to notice the all-time overall deal for the loan type you want.

What are today'southward mortgage rates?

Low mortgage rates are all the same available. Connect with a mortgage lender to find out exactly what rate you qualify for.

iToday's mortgage rates are based on a daily survey of select lending partners of The Mortgage Reports. Interest rates shown here assume a credit score of 740. See our full loan assumptions here.

Selected sources:

- https://world wide web.blackknightinc.com/category/press-releases

- https://world wide web.federalreserve.gov/monetarypolicy/fomccalendars.htm

- http://www.freddiemac.com/research/datasets/refinance-stats/alphabetize.page

The information independent on The Mortgage Reports website is for advisory purposes only and is non an ad for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Beaker, its officers, parent, or affiliates.

Source: https://themortgagereports.com/32667/mortgage-rates-forecast-fha-va-usda-conventional

0 Response to "Will the Rates Be Cut Again Soon?"

Post a Comment